The Role of Annuities in Retirement Planning

When people hear the word annuity, they often have a strong reaction. Some believe annuities are the answer to every retirement concern, while others avoid them altogether because they've heard they're expensive or complicated.

The reality is somewhere in the middle.

Like any financial tool, an annuity can be incredibly valuable in the right situation—and completely unnecessary in another. The key is understanding what an annuity is designed to do, what it costs, and whether it fits into your overall retirement income plan.

At Birch Street Financial Advisors, we don't start with products. We start with your goals. An annuity may end up being part of the solution, but it should never become the entire strategy.

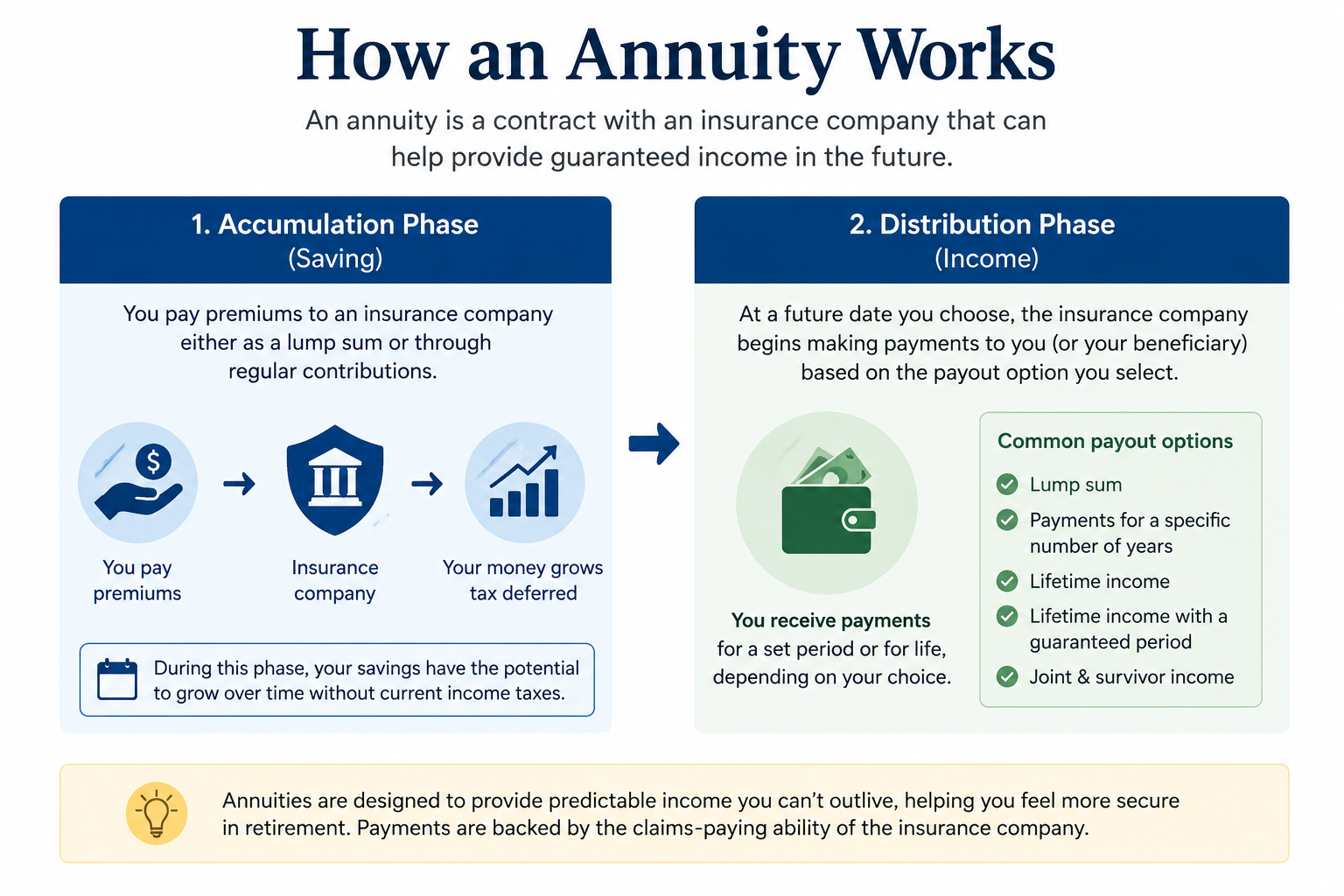

What Is an Annuity?

An annuity is a contract with an insurance company. In exchange for either a lump sum or a series of contributions, the insurance company agrees to provide future income, often for a specific number of years or even for the rest of your life.

Think of it as a way to convert part of your savings into a predictable paycheck during retirement.

For many retirees, that's appealing because retirement is often the first time in decades that regular paychecks stop arriving.

Why Some People Love Annuities

The biggest advantage of an annuity isn't necessarily higher returns. It's certainty.

Retirement introduces a number of risks that are difficult to predict:

- Living longer than expected

- Poor market returns early in retirement

- Spending too much too quickly

- Feeling anxious about withdrawing from investments

An income annuity can help reduce some of these uncertainties by providing predictable payments regardless of what the stock market is doing (subject to the financial strength and claims-paying ability of the insurance company).

For some retirees, simply knowing that their basic monthly expenses are covered provides tremendous peace of mind.

That behavioral benefit shouldn't be underestimated.

A Client Story

One client I worked with had accumulated enough investments that she could have managed retirement entirely from her portfolio.

Mathematically, the investments may have produced a higher expected long-term value.

But that's not what helped her sleep at night.

Instead, she chose to purchase an annuity with a portion of the investments because she wanted to cover her basic expenses such as her mortgage, utilities, groceries, and insurance. She wanted them to be covered by guaranteed income. She viewed the rest of her portfolio as money she could invest for growth without worrying about monthly market fluctuations.

Would every advisor have made the same recommendation? Probably not.

But retirement planning isn't just about maximizing returns—it's about helping people feel confident enough to actually enjoy retirement.

Sometimes peace of mind has value that can't be measured on a spreadsheet.

Different Types of Annuities

One reason annuities create confusion is that there isn't just one kind.

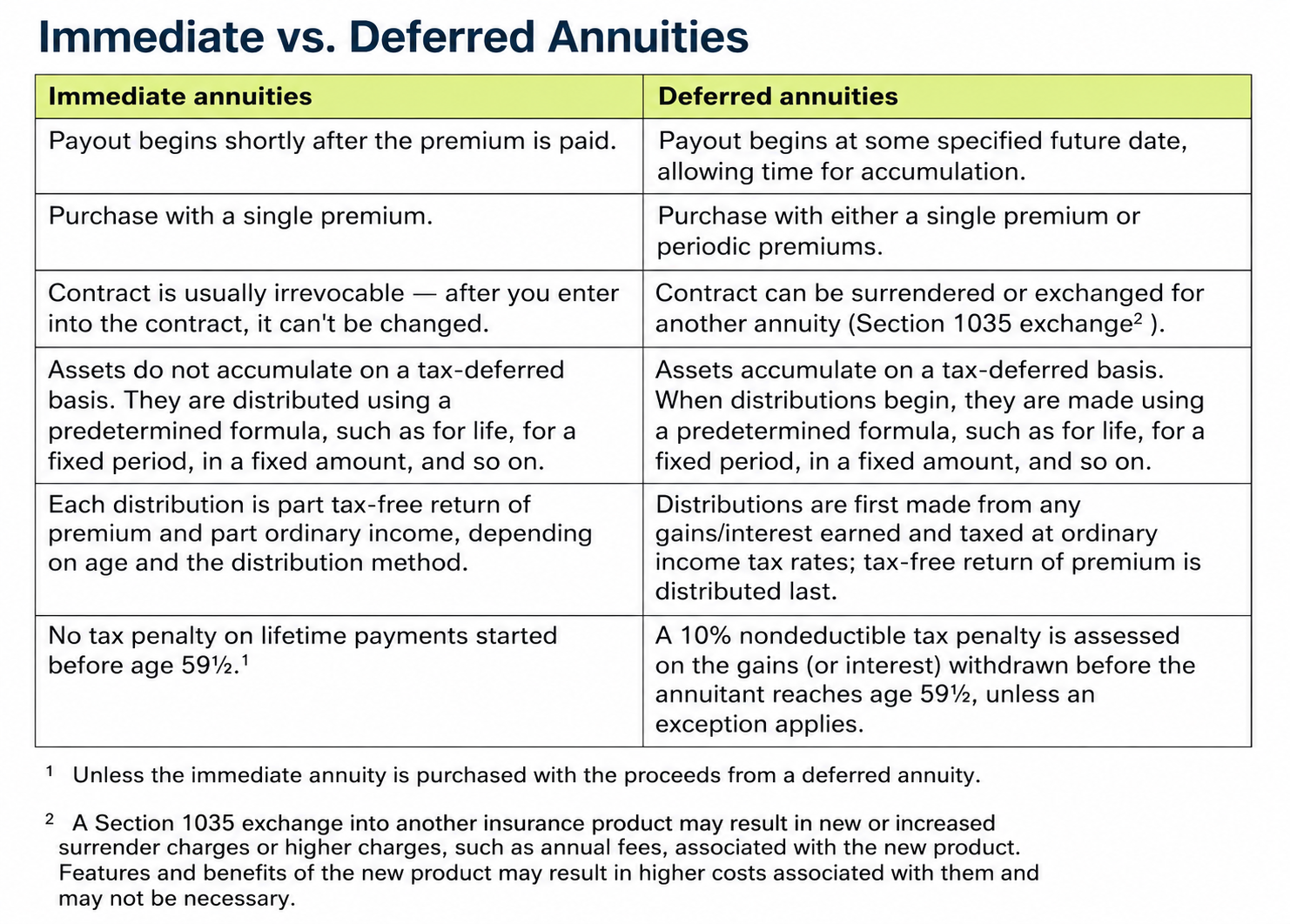

Immediate Annuities: An immediate annuity begins making income payments shortly after it is purchased. These are often used by people who are already retired and want income right away.

Deferred Annuities: Deferred annuities allow money to grow before income begins at a future date. They are more common for individuals who are still working or who don't yet need retirement income.

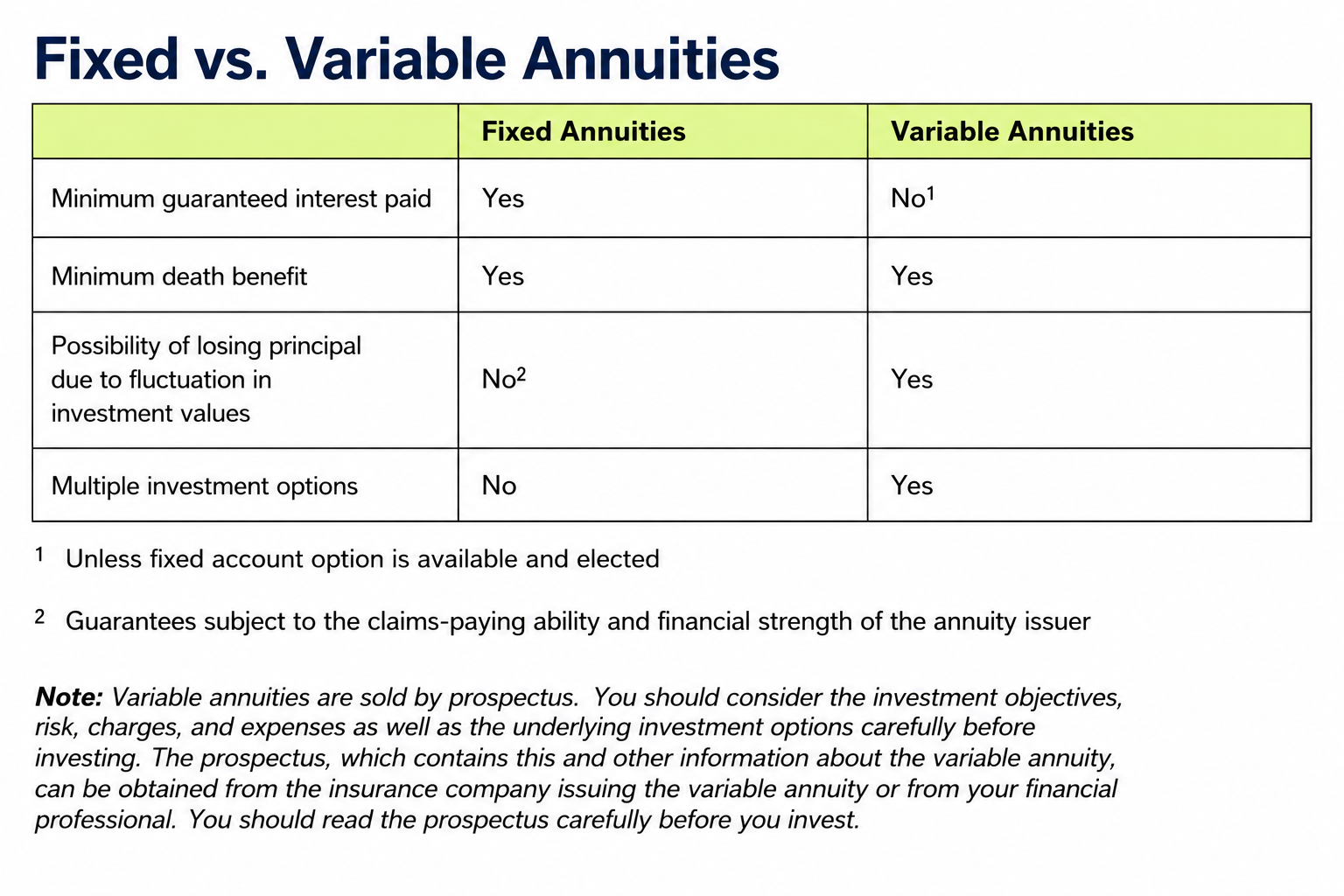

Fixed Annuities: A fixed annuity generally provides a stated interest rate or predictable payment amount, making it one of the more conservative options.

Variable Annuities: Variable annuities allow investments in market-based subaccounts. They offer greater growth potential but also greater investment risk, along with additional fees and complexity.

Indexed Annuities: Indexed annuities tie returns to a market index, such as the S&P 500, while typically providing some level of downside protection. However, participation rates, caps, spreads, and other contract features can significantly affect returns, making it important to understand exactly how the contract works.

How Can You Receive Income?

One of the most important decisions isn't simply whether to buy an annuity—it's how you receive the income.

Common payout options include:

- A lump-sum distribution

- Payments for a fixed number of years

- Lifetime income

- Lifetime income with a guaranteed minimum payment period

- Joint lifetime income for spouses

Each option involves tradeoffs between flexibility, income amount, and what happens if you or your spouse dies earlier than expected.

The Advantages

Depending on the type of annuity, potential benefits include:

- Tax-deferred growth

- No annual contribution limits

- Income that can last for life

- Ability to postpone withdrawals until needed

- Beneficiary designation that generally avoids probate

- Protection against longevity risk—the possibility of outliving your savings

For someone concerned about running out of money in retirement, these can be meaningful advantages.

The Tradeoffs

Every benefit comes with a cost.

Potential drawbacks include:

- Surrender charges if you access money too early

- Higher expenses than many traditional investments

- Investment gains taxed as ordinary income rather than capital gains

- Possible 10% IRS penalty on earnings withdrawn before age 59½ (unless an exception applies)

- Less flexibility once certain income options are elected

This is why reading the contract—and understanding the fees—is so important.

Qualified Longevity Annuity Contracts (QLACs): Planning for Later in Retirement

One specialized type of annuity that's received more attention in recent years is the Qualified Longevity Annuity Contract (QLAC).

A QLAC is a deferred income annuity purchased with money from a traditional IRA or certain employer-sponsored retirement plans. Instead of beginning payments immediately, income can be delayed until as late as age 85, creating another source of guaranteed lifetime income later in retirement.

Think of a QLAC as longevity insurance. While many retirees worry about having enough income during the early years of retirement, a QLAC is designed to help address a different concern: What if I live much longer than expected?

Income from a QLAC can help cover everyday living expenses later in life and may also provide additional cash flow during the years when healthcare and long-term care costs often increase. While a QLAC is not long-term care insurance, it can be one component of a broader strategy for managing expenses later in retirement.

Another potential benefit is tax planning. Under current IRS rules, eligible retirement assets used to purchase a QLAC are excluded from required minimum distribution (RMD) calculations until annuity payments begin, subject to IRS limits. For some retirees, this can provide additional flexibility when managing taxable income in the early years of retirement.

Don't Forget Inflation

One of the biggest considerations when evaluating an annuity is inflation.

Many private annuities pay a fixed dollar amount for life. While that income is predictable, its purchasing power declines over time as living costs increase.

For example, a monthly payment that comfortably covers expenses at age 65 may not stretch nearly as far at age 85.

Some pensions, particularly many government pensions, include cost-of-living adjustments (COLAs), but most private annuities do not.

That's why I rarely think of guaranteed income in isolation. It should be coordinated with investment assets that have the potential to grow over time and help offset inflation.

Annuities Work Best as Part of a Plan

One mistake I see is evaluating an annuity by itself.

Instead, I ask questions like:

- Which expenses absolutely must be covered every month?

- How much guaranteed income already exists from Social Security or a pension?

- How much flexibility does the client want?

- How comfortable are they with market fluctuations?

- What legacy goals do they have?

Sometimes the answer is no annuity at all.

Sometimes the answer is allocating only a portion of retirement assets to guaranteed income while investing the remainder for long-term growth and flexibility.

The right answer depends on the person—not the product.

Final Thoughts

Annuities are neither inherently good nor inherently bad.

Annuities are simply one tool available to help solve a very specific retirement problem: creating reliable income that you can't outlive.

For some retirees, that certainty provides confidence and peace of mind. For others, maintaining liquidity and investment flexibility is more valuable.

The most effective retirement income strategies rarely rely on a single solution. Instead, they thoughtfully combine guaranteed income, investment growth, tax planning, Social Security optimization, and ongoing adjustments as life changes.

As with most areas of financial planning, the goal isn't to find the "best" product. It's to build the strategy that best supports the retirement you want to live.

How Birch Street Financial Advisors Can Help

Choosing whether to include an annuity in your retirement plan isn't about buying a product—it's about building a retirement income strategy that fits your goals.

At Birch Street Financial Advisors, we evaluate annuities within the context of your complete financial picture. We help clients coordinate guaranteed income with Social Security, pensions, investment portfolios, tax planning, Roth conversion opportunities, Medicare premiums, estate planning goals, and long-term retirement spending needs. We also help clients compare existing annuity contracts, understand fees and surrender provisions, and determine whether an annuity still fits their overall plan.

Our goal isn't to recommend an annuity for every client. It's to help you understand the tradeoffs, make informed decisions, and create a retirement income plan that aligns your money with what matters most.