OBBBA & Charitable Deductions: What’s Changing—and What’s Staying the Same

Signed into law on July 4, 2025, the One Big Beautiful Bill Act (OBBBA) reshapes how charitable contributions are deducted, starting in 2026. While the intent is to modernize the rules and make giving more consistent across income levels, these changes also make it more important to plan your gifts thoughtfully—timing, structure, and documentation all matter.

Below, we explore what’s new under OBBBA, what’s staying the same, and how you can adjust your giving strategy to stay both generous and tax-smart.

What’s New for 2026

1. A New 0.5% AGI Floor for Itemized Charitable Deductions

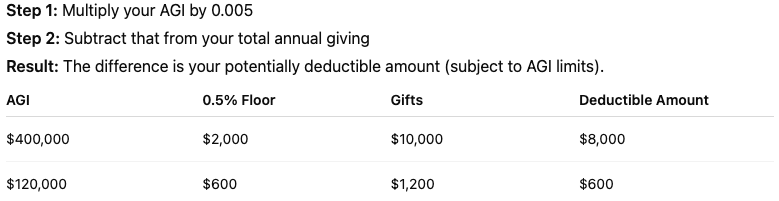

Starting in 2026, taxpayers who itemize can only deduct charitable contributions that exceed 0.5% of adjusted gross income (AGI). In practice, this means that the first $500 of donations per $100,000 of income won’t be deductible.

For example, if your AGI is $400,000, you’ll need to give more than $2,000 before any of your contributions count toward your itemized deductions.

You can refer to this AGI Floor Calculator to determine your personal limitations:

AGI Floor Calculator

Planning idea: Consider bunching several years’ worth of gifts into one tax year so you clear the 0.5% floor and meaningfully increase your deduction. Contributing appreciated stock or other non-cash assets can help you reach the threshold faster while avoiding capital gains tax. Establishing or adding to a donor-advised fund (DAF) in 2025 can also allow you to claim the full deduction under current rules and then spread your giving out over time.

“Think strategically—2025 may be your last chance to claim a full deduction before the new floor applies.”

2. A Universal “Above-the-Line” Deduction for Non-Itemizers

For those who take the standard deduction, OBBBA brings back a universal charitable deduction starting in 2026. Taxpayers will be able to deduct up to $1,000 (single) or $2,000 (married filing jointly) for cash gifts made directly to qualified public charities.

This deduction cannot be claimed for gifts to donor-advised funds or private foundations, but it does provide a modest incentive for the roughly 90% of taxpayers who don’t itemize.

Planning idea: If you don’t typically itemize, consider setting up recurring cash gifts to qualified charities to capture this annual deduction. Even small, regular donations can help maximize this benefit while supporting the causes you value most.

3. Cap on Charitable Deduction Value for High-Income Taxpayers

Taxpayers in the 37% federal tax bracket will see their charitable deduction benefit capped at 35%, beginning in 2026. Your donations will still count in full, but the tax savings will be slightly smaller. For example, a $10,000 gift that currently reduces your tax bill by $3,700 will be limited to $3,500.

Planning idea: If you’re in the top bracket, front-load larger gifts before the end of 2025 to take advantage of the full deduction value before the cap applies. This may be especially beneficial if you expect your income to remain high in future years.

4. A New 1% Floor for Corporate Giving

Businesses structured as C-corporations will only be able to deduct the portion of charitable contributions that exceeds 1% of taxable income beginning in 2026.

Planning idea: If you own a C-corp, evaluate whether giving personally—or donating appreciated business assets through a DAF—offers a better tax outcome.

5. 2025: A Critical Year for Planning Ahead

Because the new rules begin in 2026, 2025 represents a valuable planning window. If you’re considering significant charitable gifts in the next few years, acting now allows you to:

- Deduct 100% of qualifying donations without the 0.5% floor.

- Lock in the current 37% deduction value if you’re in the top bracket.

- Front-load contributions to a DAF, allowing you to give strategically over time under more favorable tax conditions.

“2025 is your window to lock in higher deduction value before the rules tighten.”

What’s Staying the Same

Even with OBBBA’s updates, several long-standing charitable giving provisions remain intact—preserving valuable opportunities for those who plan carefully.

1. The 60% of AGI Limit for Cash Gifts to Public Charities

The ability to deduct cash gifts up to 60% of AGI to qualified public charities continues. This higher cap (increased from 50% under prior law) allows more flexibility for large donations in a single year.

Gifts of appreciated property or contributions to private foundations remain subject to lower limits (generally 30% of AGI). If you exceed these limits, you can carry forward unused deductions for up to five years.

Planning idea: Use this generous 60% rule strategically—particularly when your income is high or you’re selling a business or property. Pairing cash donations with appreciated securities can help you diversify your charitable strategy while optimizing tax results.

2. Carryforwards for Excess Charitable Deductions

If your charitable contributions exceed the annual AGI limit, you can carry the unused portion forward for up to five tax years. This allows for multi-year giving flexibility, especially when bunching large gifts into one year.

Planning idea: Keep a running summary of your charitable carryforwards and confirm that each gift was properly documented (see substantiation rules below). Coordinate with your tax preparer to ensure prior-year carryovers aren’t lost.

3. Qualified Charitable Distributions (QCDs) from IRAs

OBBBA does not change the rules for Qualified Charitable Distributions (QCDs). Individuals aged 70½ or older can continue to make up to $108,000 per year (2025 limit) and $111,000 (2026 limit) in direct IRA gifts to qualified charities, satisfying part or all of their required minimum distribution (RMD) without increasing AGI.

Planning idea: QCDs remain one of the most tax-efficient ways for retirees to give. Because they reduce taxable income (rather than creating an itemized deduction), they’re unaffected by the new 0.5% AGI floor or deduction caps.

“QCDs bypass the new charitable deduction floor entirely—making them even more valuable for retirees.”

Documentation and Substantiation: What You Must Keep

Regardless of which rules apply, good recordkeeping is non-negotiable. To claim any charitable deduction, you must have contemporaneous written acknowledgment from the charity for each contribution of $250 or more.

Each acknowledgment should include:

- The amount donated (or a description if it’s a non-cash gift)

- A statement confirming whether goods or services were received in exchange

- The estimated value of any benefits (if applicable, such as a gala ticket or dinner)

For non-cash contributions:

- Keep a record of the items, condition, and fair-market value.

- Complete Form 8283 for non-cash gifts over $500.

- Obtain a qualified appraisal for donations over $5,000 (except publicly traded stock).

For DAF contributions, retain the contribution acknowledgment from the sponsoring organization showing the date, value, and confirmation of your irrevocable gift. Grants distributed later from your DAF don’t generate additional deductions, but your original contribution substantiates your tax benefit for that year.

Even small cash donations require bank or credit card records. Keeping these organized ensures your generosity holds up under IRS review—and makes year-end tax planning smoother.

Charitable Gift Recordkeeping Checklist

- Written acknowledgment for all gifts of $250+

- Description and valuation for non-cash donations

- Complete Form 8283 for gifts > $500

- Appraisal for non-cash gifts > $5,000

- Bank/credit card proof for all cash gifts

The Bottom Line

OBBBA doesn’t reduce the importance—or the impact—of charitable giving. It simply changes the rules of the game. The key to maximizing both your philanthropic and tax outcomes lies in being proactive: bunching gifts strategically, coordinating timing with income, and keeping impeccable documentation.

“With the right planning, your generosity can still align beautifully with your financial goals—and the life you want to build.”