The Backdoor Roth IRA — A Workaround Worth Understanding

What Is a Backdoor Roth IRA?

A backdoor Roth IRA isn’t a special type of account—it’s a strategy.

It was designed to solve a very specific problem: higher-income earners are often phased out of making direct Roth IRA contributions. Once income exceeds certain IRS thresholds, the ability to contribute directly disappears. The backdoor Roth creates an alternative path.

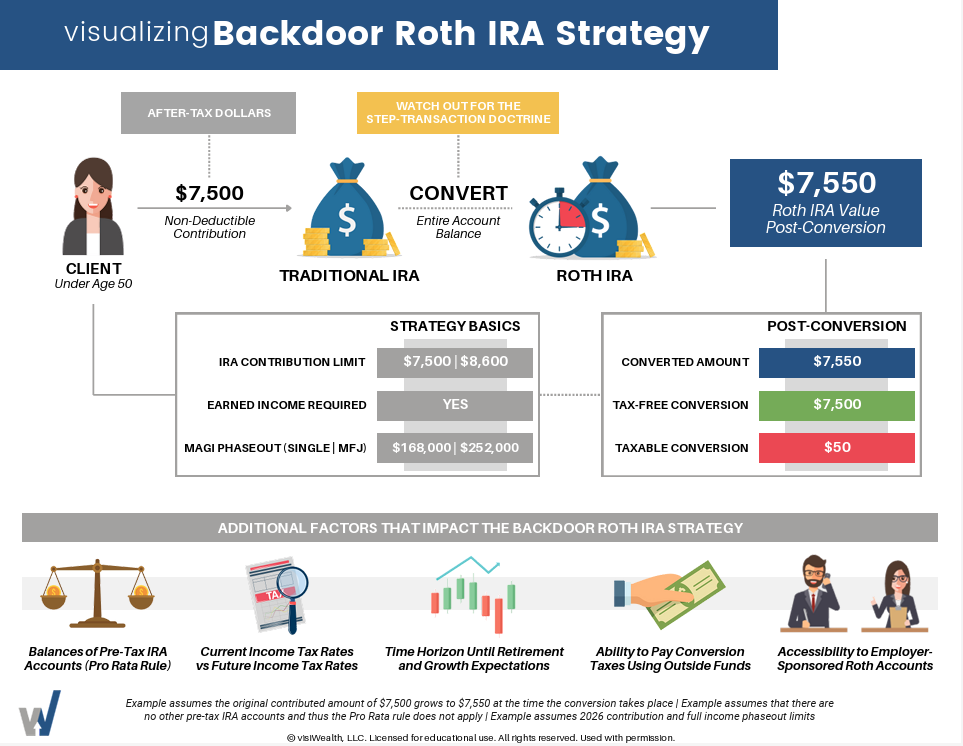

At its core, the strategy involves making a non-deductible (after-tax) contribution to a traditional IRA and then converting that balance to a Roth IRA. It’s a simple concept, but like most tax strategies, the details matter.

How the Strategy Works

The process typically unfolds in two steps.

First, you make a non-deductible contribution to a traditional IRA. For 2026, contribution limits are $7,500 per year, or $8,600 if you’re age 50 or older, assuming you have sufficient earned income.

Next, you convert those funds to a Roth IRA. Ideally, this happens relatively soon after the contribution is made to minimize any earnings that could be taxable. At the same time, it’s important that the steps are handled properly and documented clearly, so the transaction stands on its own and is not challenged as a single integrated step.

When executed cleanly—and in the absence of other complicating factors—the result is often minimal tax impact. For example, if a $7,500 contribution grows slightly before conversion, only that small amount of growth would be taxable. Once the funds are in the Roth, future growth and qualified withdrawals can be entirely tax-free.

Why This Strategy Exists

Income limits are what create the need for this strategy in the first place.

For 2026, direct Roth IRA contributions begin to phase out at $168,000 for single filers and $252,000 for married filing jointly. Beyond those levels, the ability to contribute directly is eliminated.

The backdoor Roth IRA exists as a workaround—an indirect way for higher earners to still access Roth savings despite those limits.

Where the Details Matter

This is where the strategy becomes more nuanced.

One of the most important considerations is the pro-rata rule. If you have existing pre-tax IRA balances—such as traditional, SEP, or SIMPLE IRAs—the IRS views all IRA assets as one combined pool. That means part of your conversion may be taxable, even if your intention was to convert only after-tax dollars.

This is why we often look closely at IRA balances as of year-end. Even small existing balances can impact the effectiveness of the strategy.

There’s also a timing element. Converting soon after contributing can help minimize taxable earnings, but it’s equally important that the steps are executed thoughtfully and reported correctly.

Backdoor Roth vs. Taxable Investing

For many clients, the real decision isn’t whether they can do a backdoor Roth—it’s whether they should, instead of simply investing additional dollars in a taxable account.

Taxable accounts offer flexibility, but they come with ongoing taxation. Dividends, interest, and realized gains all create tax drag over time.

A Roth IRA offers a different outcome. Once funds are inside the account, they grow without ongoing taxation, and qualified withdrawals in retirement are tax-free. Over time, that difference can create meaningful flexibility—especially when managing income in retirement or navigating tax brackets, Medicare premiums, or Social Security taxation.

When It Makes Sense

The backdoor Roth IRA tends to be most valuable for individuals who are above the income thresholds for direct Roth contributions and are looking to build tax diversification.

It’s often particularly attractive for clients who are earlier in their high-earning years and still have a long time horizon. The longer the runway, the more opportunity there is for tax-free compounding to work in their favor.

It can also be a useful strategy for those who expect to be in the same—or even higher—tax brackets in the future. In those cases, paying tax today in exchange for tax-free growth later can be a compelling tradeoff.

Planning Pointers

This is one of those strategies where the surrounding context matters just as much as the mechanics.

Existing IRA balances are often the first place to look, since they can significantly impact the outcome due to the pro-rata rule.

There’s also a broader conversation around current versus future tax rates. While Roth strategies are often appealing, they tend to be most effective when future tax rates are expected to be higher—whether due to rising income or potential legislative changes.

Time horizon plays a role as well. The longer the investment period, the more valuable tax-free growth becomes. For clients closer to retirement, the benefits may be more limited, depending on how the funds are expected to be used.

And in cases where a conversion does trigger some tax, it’s generally best to pay that tax from outside funds rather than using IRA dollars. This allows more money to remain in the Roth, where it can continue compounding tax-free.

There are special rules on reporting the conversions to the IRS form 8606 so these rules need to be reviewed.

Use this link for a simplified visual on how to determine if a Backdoor Roth is right for you.

A Note on Alternatives

It’s also worth stepping back and considering the full picture.

For some clients, an employer-sponsored Roth option—such as a Roth 401(k)—may be a simpler and more efficient path. These plans don’t have income phaseouts and allow for significantly higher contribution limits.

The backdoor Roth IRA is valuable, but it’s not always the first or best option. It’s one piece of a broader planning strategy.

Final Thought

The backdoor Roth IRA is a thoughtful workaround to a very specific limitation in the tax code.

It’s not complicated once you understand the steps—but it does require coordination, awareness of the details, and a clear sense of how it fits into your overall plan.

When used intentionally, it can create something that’s increasingly valuable over time: a pool of assets that grows free from future tax uncertainty.