When Fed Leadership Changes: What It Really Means for Interest Rates and Inflation

Whenever there is a potential change in Federal Reserve leadership, headlines intensify and market commentary accelerates. It’s natural to wonder whether a new Fed Chair will mean lower interest rates, higher inflation, or a dramatic shift in policy direction.

But before reacting to personalities, it helps to understand structure.

The Federal Reserve operates under the Federal Reserve Act of 1913, and its modern mandate was clarified by the Humphrey-Hawkins Act of 1978. The Fed’s dual mandate is clear: promote price stability and maximum employment. The Chair plays an important leadership role, but monetary policy decisions are made by the Federal Open Market Committee (FOMC), a 12-member voting body. No single Chair can set rates unilaterally.

Recent news noted President Trump’s intention to nominate Kevin Warsh to succeed Jerome Powell when Powell’s term expires in mid-May. Warsh would require Senate confirmation, and Powell could technically remain on the Board until January 2028 if he chose to. While leadership transitions can influence tone and communication style, history suggests they rarely create abrupt policy shifts without economic justification.

And that brings us to what truly drives interest rates: data.

The Inflation Backdrop

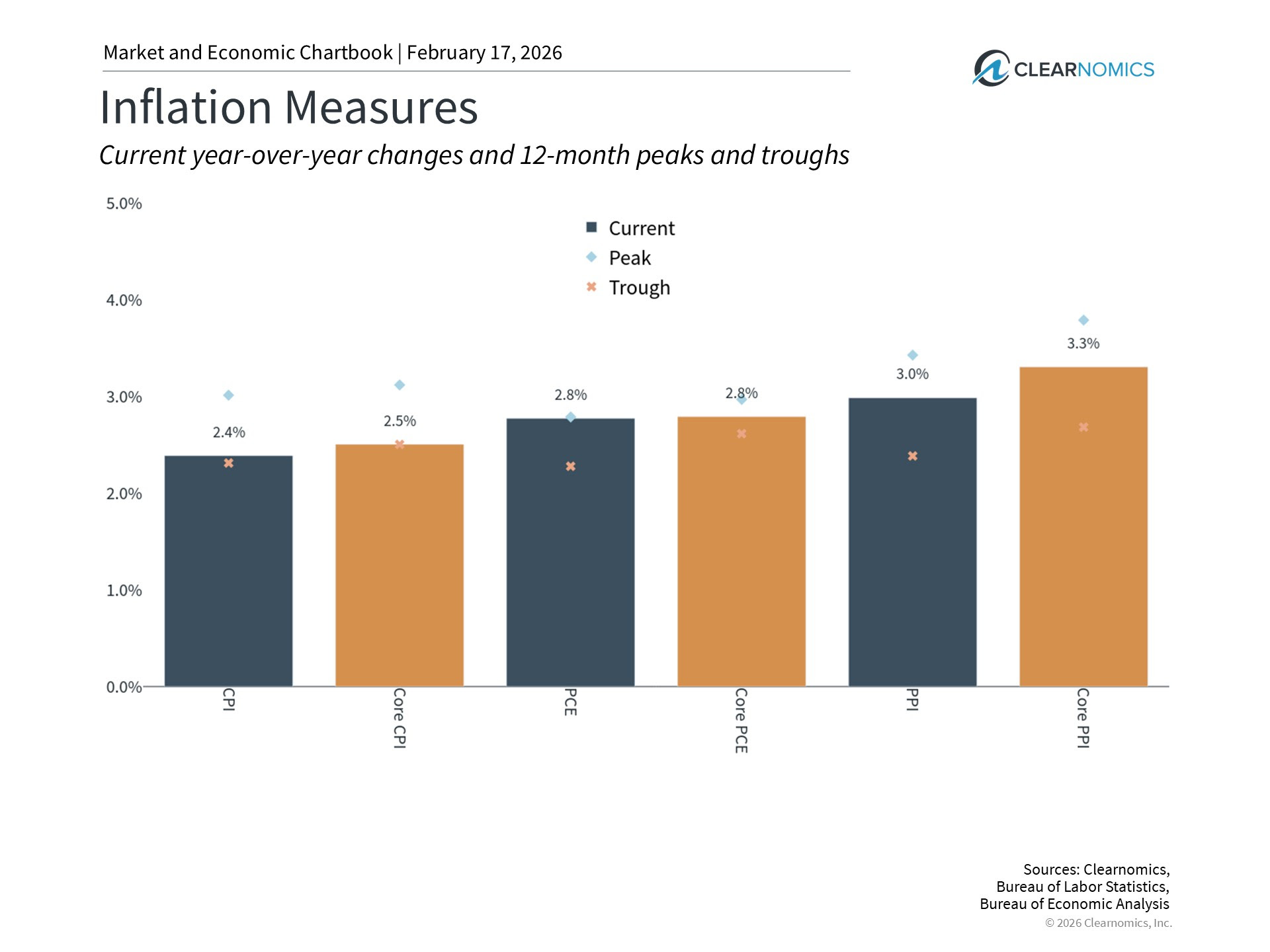

The most recent inflation readings show continued moderation. Consumer prices rose 2.4% year-over-year, below expectations and down from 2.7% in December. Core CPI rose 2.5%, while “supercore” inflation — which excludes food, energy, and shelter — rose just 2.1%. The federal funds rate has already declined from its peak of 5.25% to 3.50%, and the 10-year Treasury yield has moved back toward 4.0%.

This Clearnomics chart reinforces this broader theme. CPI is running at 2.4%, Core CPI at 2.5%, PCE and Core PCE at 2.8%, and producer prices slightly higher but well below prior cycle peaks. These readings are far from the inflation surge of 2022 and are moving closer to the Fed’s long-term 2% objective.

When inflation data comes in below expectations, markets adjust quickly. After the latest CPI report, Treasury yields declined across the curve because investors reduced the probability that rates would need to remain restrictive for an extended period. Fed funds futures currently reflect expectations for one potential cut in July and possibly two across 2026.

Notice the pattern: markets reacted to inflation data, not to leadership headlines.

Would a New Chair Automatically Mean Lower Rates?

It is tempting to assume that a Chair perceived as more “dovish” would quickly push rates lower. In reality, the Fed directly controls only very short-term rates through the federal funds rate. Long-term interest rates — including mortgage rates — are influenced by inflation expectations, economic growth, Treasury issuance, and global capital flows.

If markets believed rate cuts were coming too quickly while inflation remained above target, long-term yields could actually rise. This would steepen the yield curve and potentially offset short-term policy easing. In other words, credibility matters as much as policy direction.

The Fed’s institutional structure exists specifically to preserve that credibility. Governors serve staggered 14-year terms, and monetary policy decisions require consensus. This design reduces the likelihood of dramatic swings based solely on political changes.

The Bigger Picture for Investors

Since 1950, markets have navigated numerous Fed Chairs, recessions, inflation spikes, and policy regimes — from double-digit rates in the early 1980s to near-zero rates after the financial crisis. Through each period, long-term disciplined investors were rewarded not because they predicted policy shifts perfectly, but because they remained aligned with enduring economic growth.

Right now, inflation is moderating. The policy rate has already come down meaningfully from its peak. Markets are anticipating gradual additional easing. None of these developments hinge on one individual; they reflect economic conditions.

At Birch Street, our focus remains where it belongs: positioning portfolios thoughtfully across interest rate environments, managing duration in alignment with cash flow needs, and integrating tax-efficient strategies into long-term planning.

Leadership changes may shape headlines. Inflation data shapes policy. And disciplined strategy shapes outcomes.